[Case study]

DEX:

Enabling money movement for the unbanked population

for banco azteca, Central America

user research

product strategy

sketching

wireframing

prototyping

functional documentation

Project: Product strategy and design for a money movement mobile app in Mexico.

Problem statement: Over the course of 10 weeks, we worked with Banco Azteca’s Dinero Express (DEX) division to help them transform their business from supporting customers in brick and mortar stores to becoming the ultimate digital money movement platform in Central America. This was an urgent business need as the company was falling severely behind new players in the field who were heavily attracting the younger tech-savvy generation over DEX.

Process: To understand the user and market context in Mexico, we started with field research as well as stakeholder interviews. We used our learnings to define how DEX needs to position itself and created a product strategy based on insights from the field. We designed key flows and architecture of the Android app. To ensure the product was built right, I produced documentation for client team. This documentation showed our platform agnostic approach, enabling client to also develop their iOS app easily.

My role and responsibilities: I worked closely with a creative lead, two visual designers, a researcher and a strategist. I led the interaction design track, creating all artifacts (wireframes, flows, prototypes etc.).

Final product snapshot

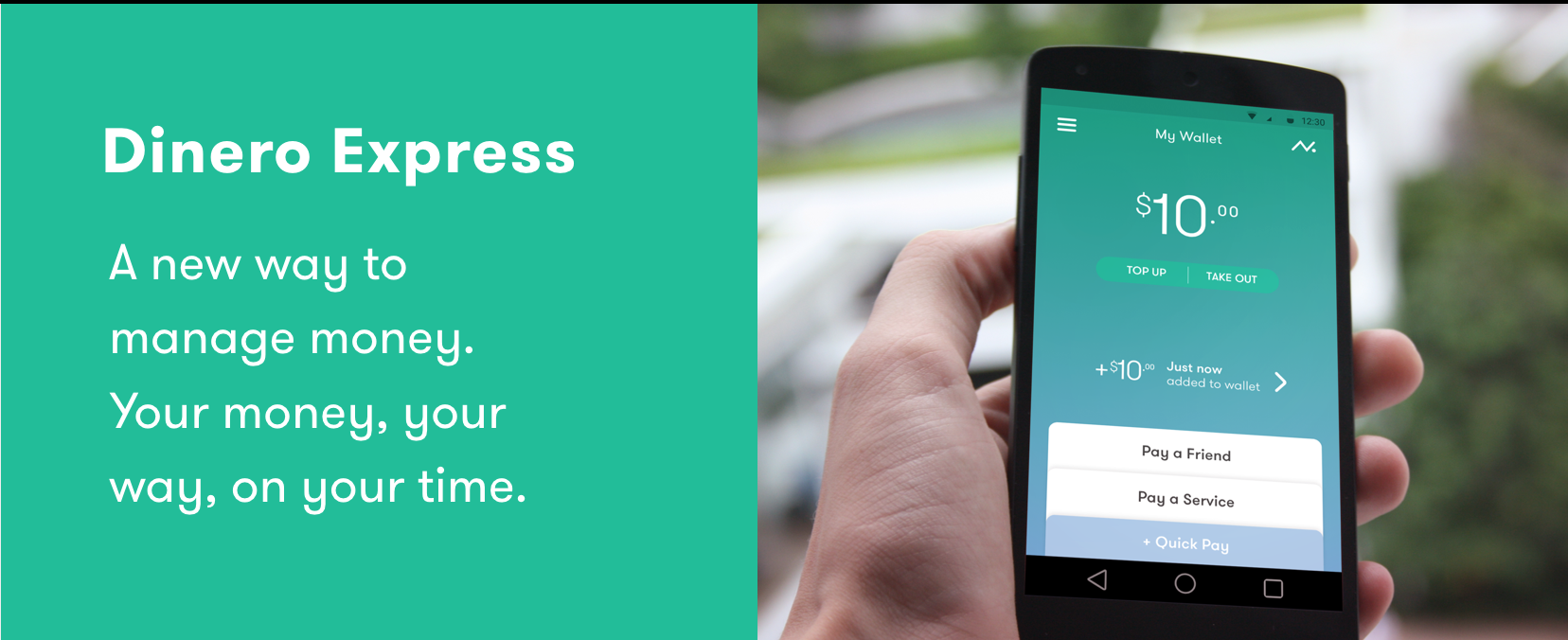

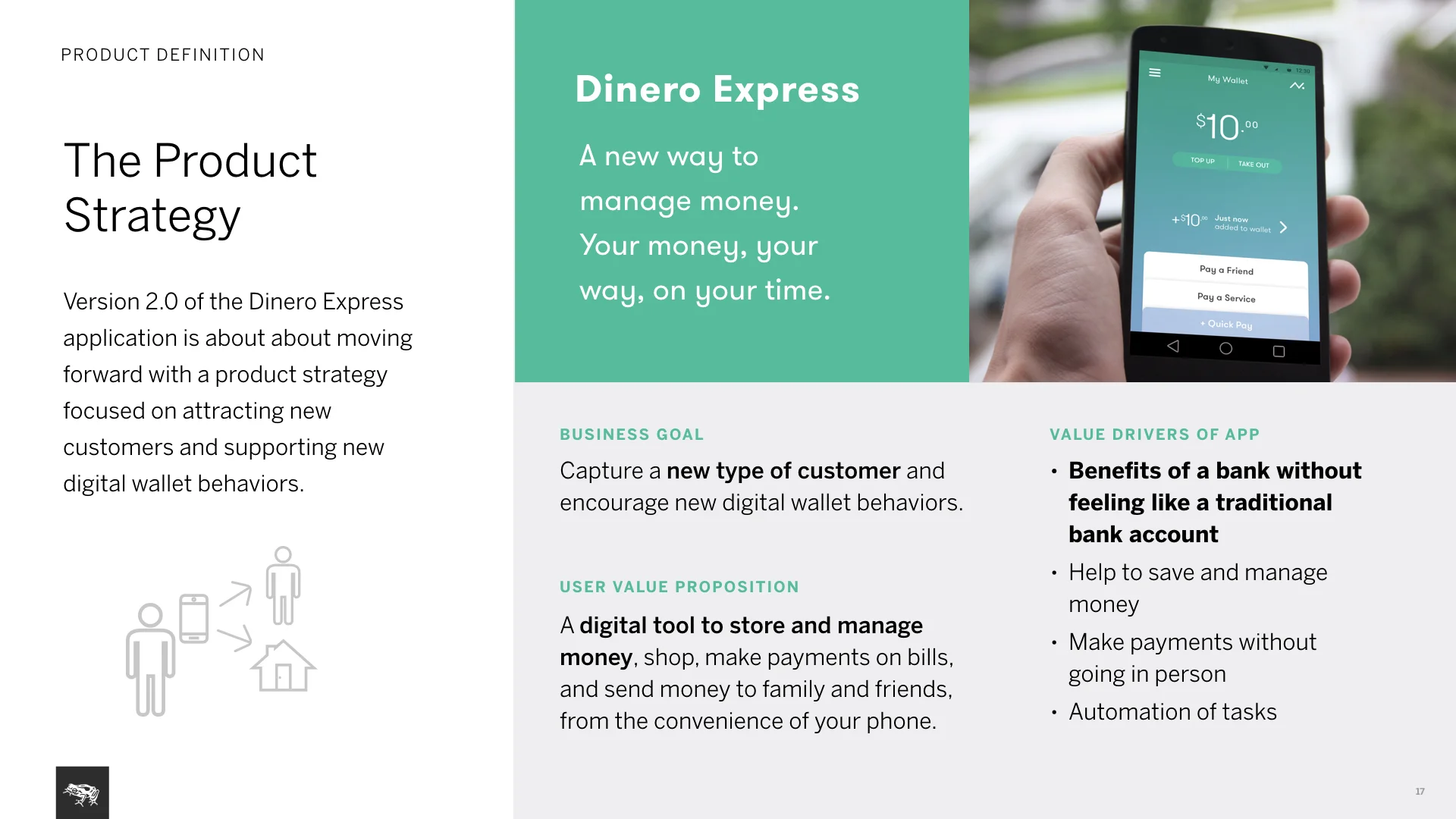

DEX, a secure and personal digital wallet featuring user’s balance, latest transactions alongside key actions. Main business goal is attracting new types of customers. For users, it is a new way to manage money, keeping it secure and accessible digitally without the need for a bank account, and most importantly with the ability to send/spend it as they wish.

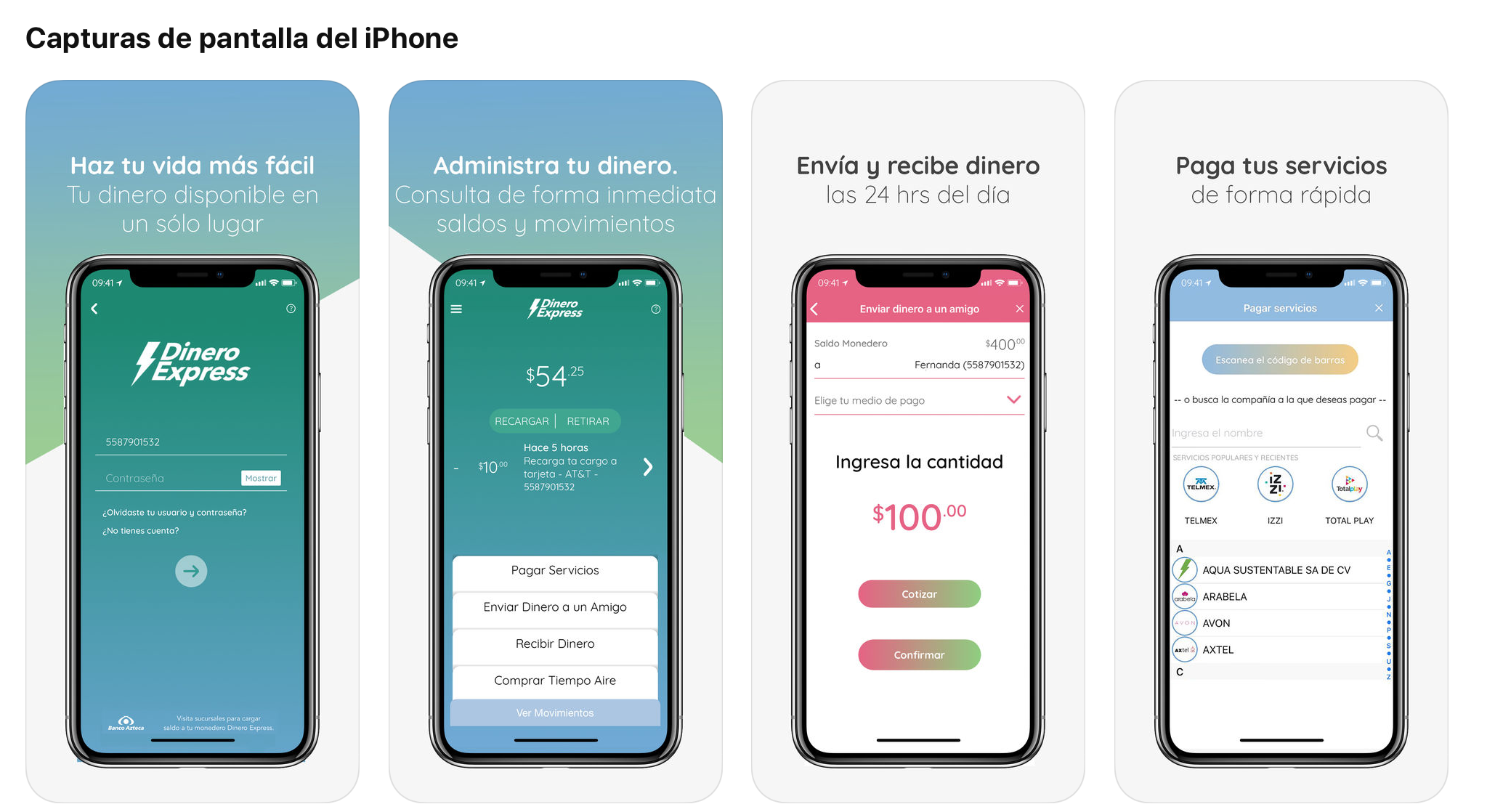

Android and iOS apps have been developed by the client and are on the Mexican app stores. Google play link, Apple app store link

Project highlights

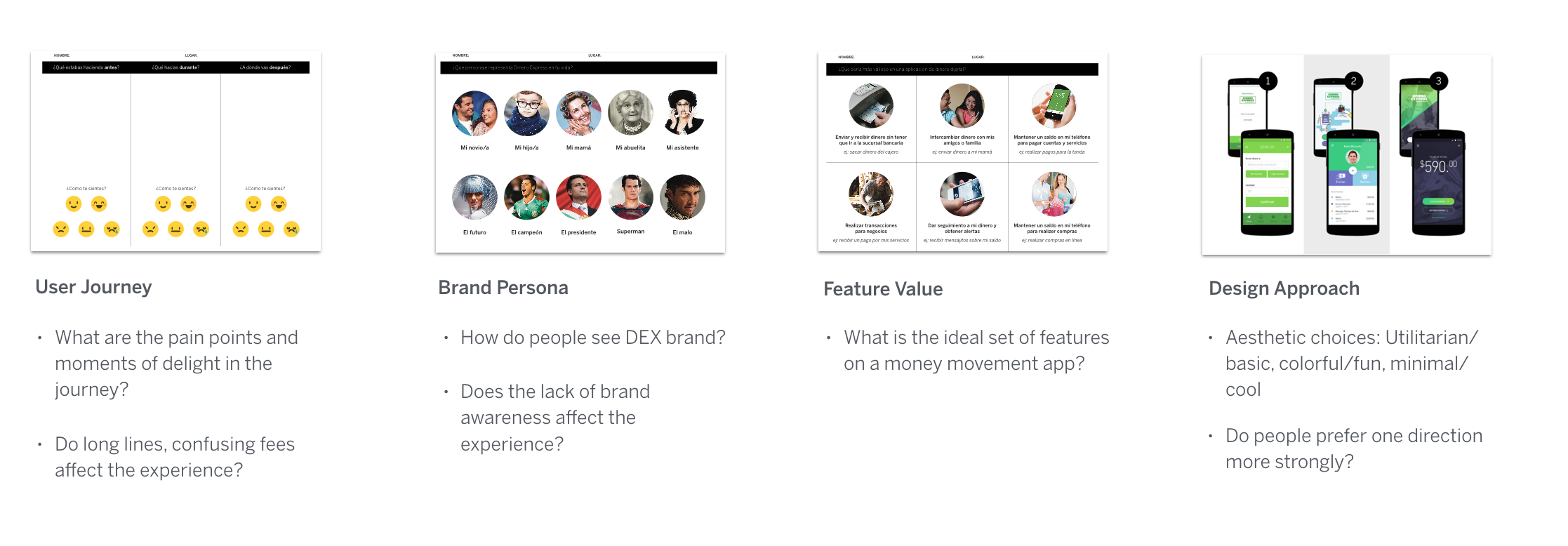

field research to debunk initial hypothesis and explore the right user insights

As we were prepping for the field, we started developing early hypothesis on pain points such as excruciatingly long lines in stores and lack of distinguished DEX brand in retail stores. We structured our research around confirming these and conducting participatory design exercises with participants.

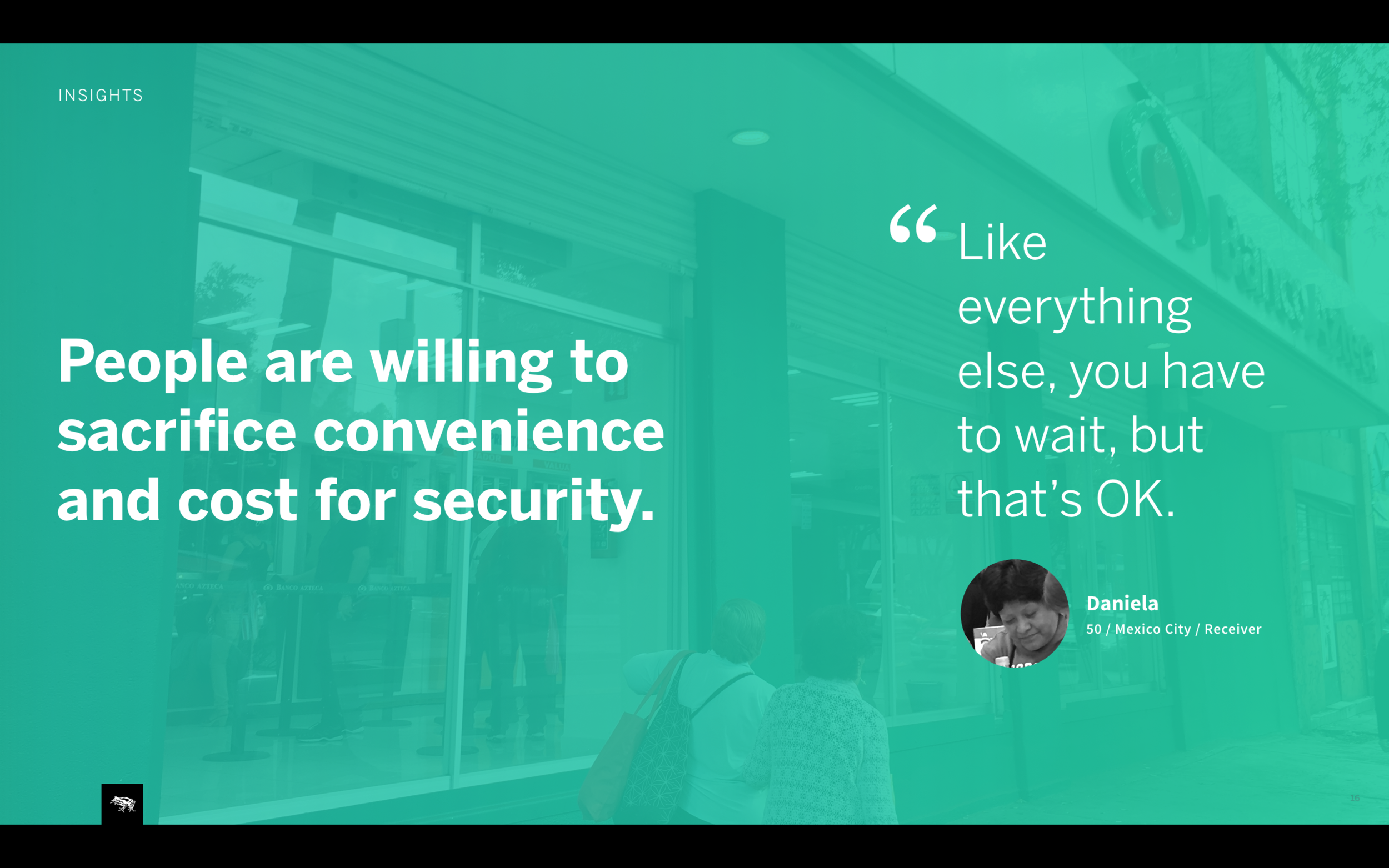

As soon as we were in the field, some of those early hypothesis started breaking. For instance, people did not care about the excruciatingly long lines. They simply accepted it as “Just something you have to do”. They mainly cared that the money got to their families fast and secure. They also did not care about lack of branding, solely focusing on utility of the store. Some of the insights I want to highlight:

Major mistrust in institutions are part of everyday life and dictate how people think about money. Many participants hesitated to discuss their own financial choices, assuming it may affect them somehow. We needed to make the product induce user trust first and foremost.

People desire transparency and control over their money. Participants repeatedly mentioned pain of not knowing status of money sent/received. In remote parts of Mexico, it was typical for a family member to travel long distances only to learn money was not yet received. We needed to create a product with clear instructions, status and record of money movement to ease the user.

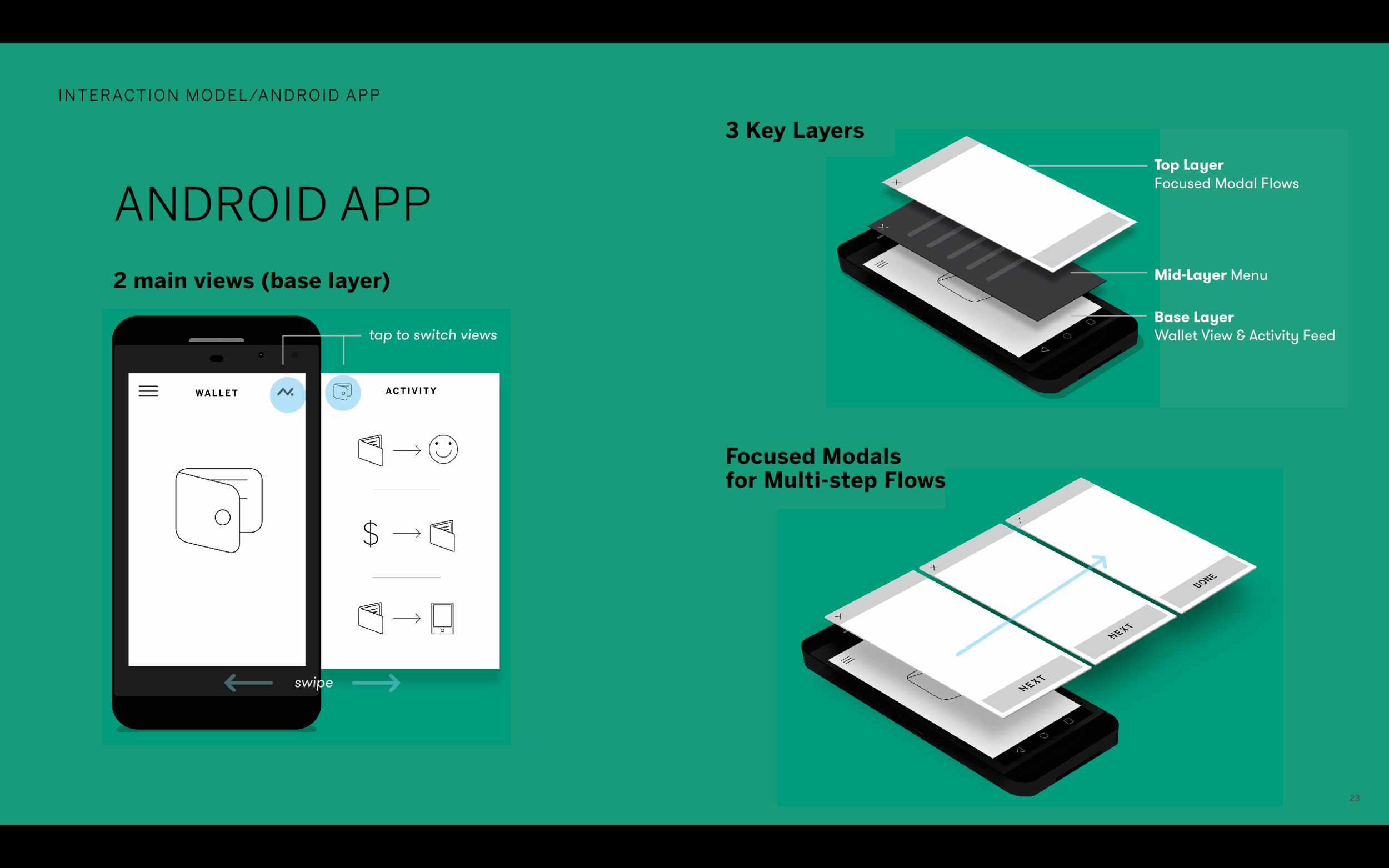

2. How to apply learnings into the product

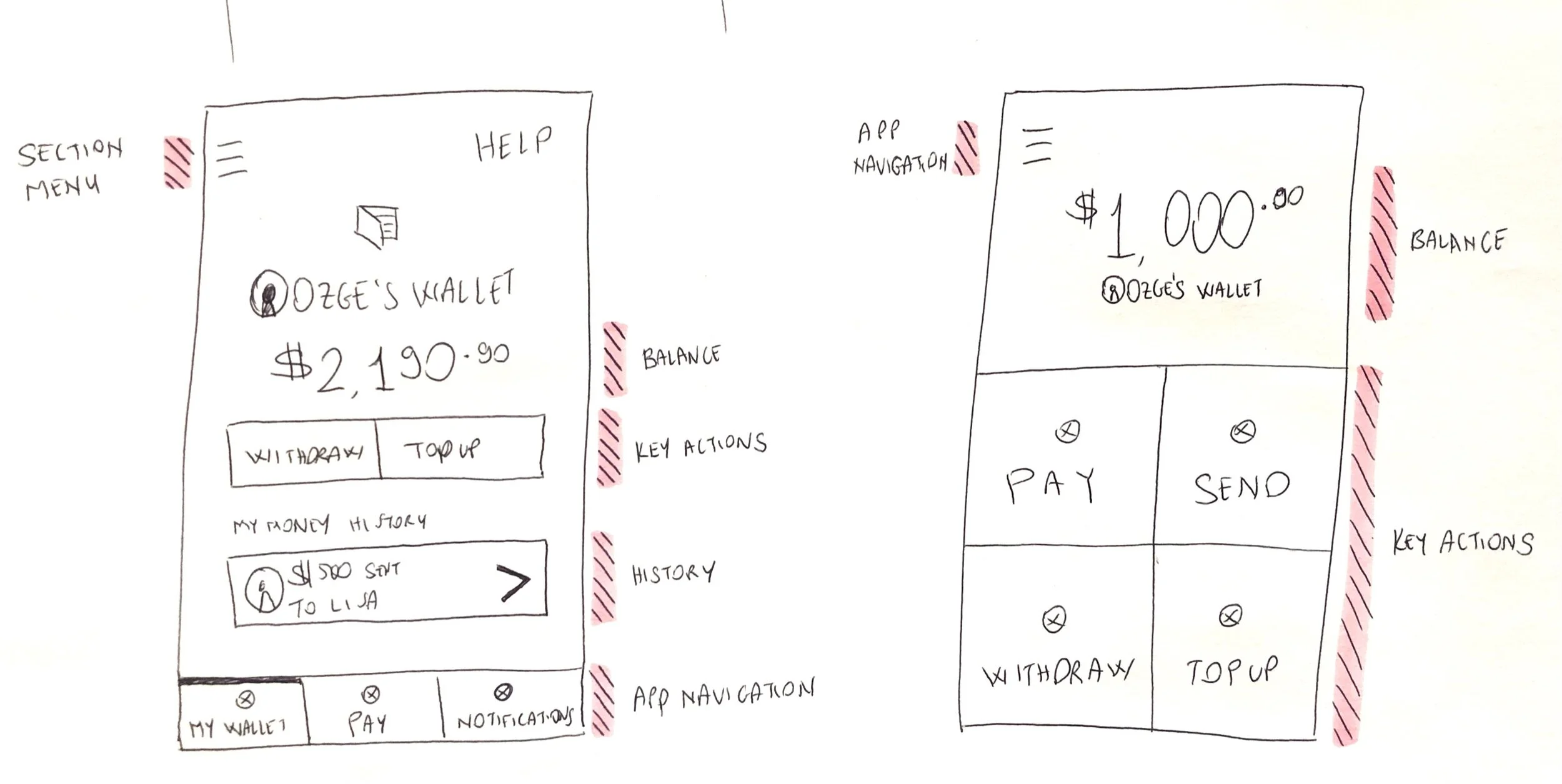

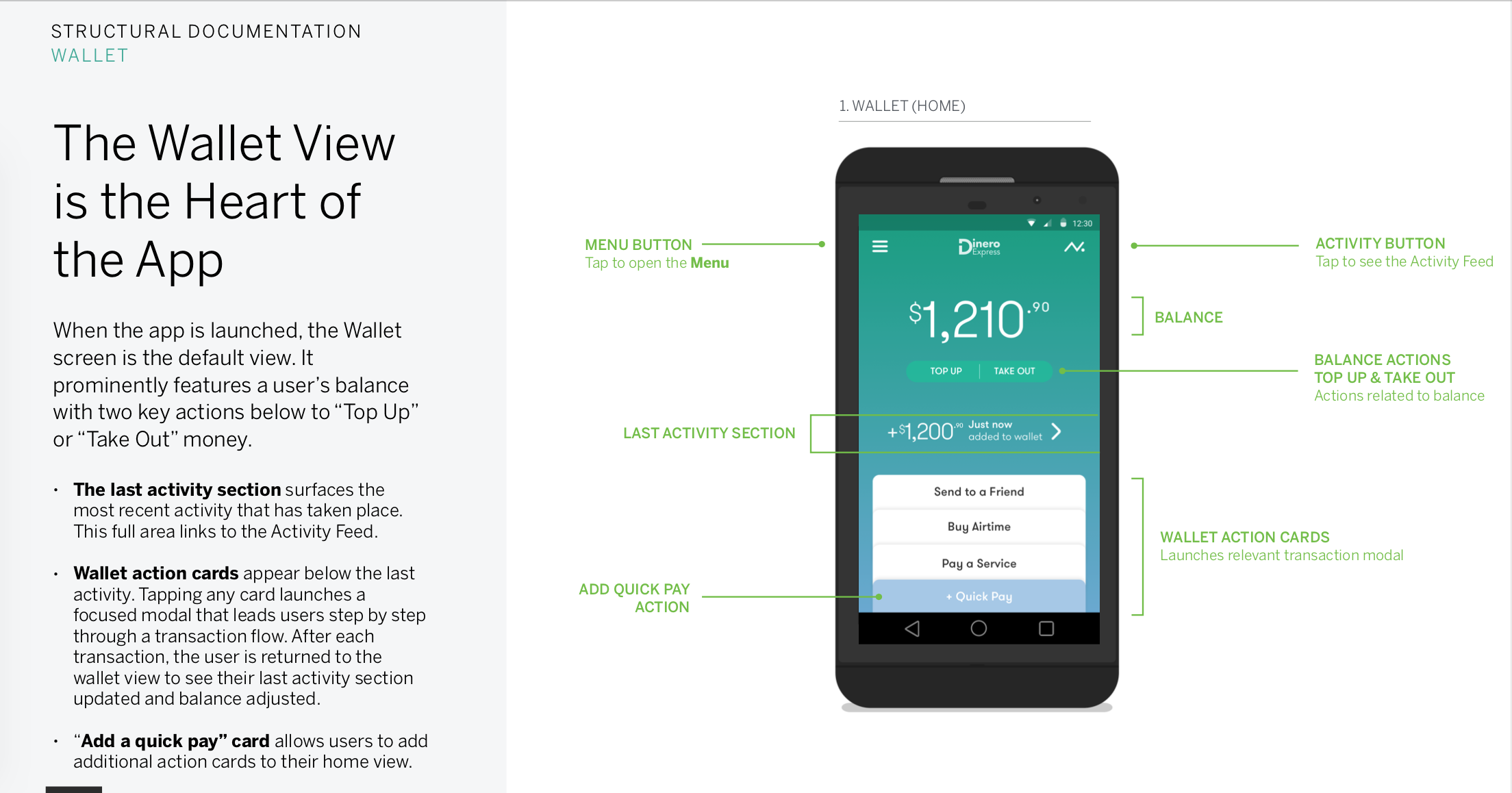

On initial sketches, I explored various models: from a skeuomorphic concept of a wallet to a utilitarian one focused on quick actions. We decided to go for a simple concept that felt familiar to users, featuring users’ balance and key wallet actions stacked to resemble cards in a physical wallet.

Building trust by providing transparency

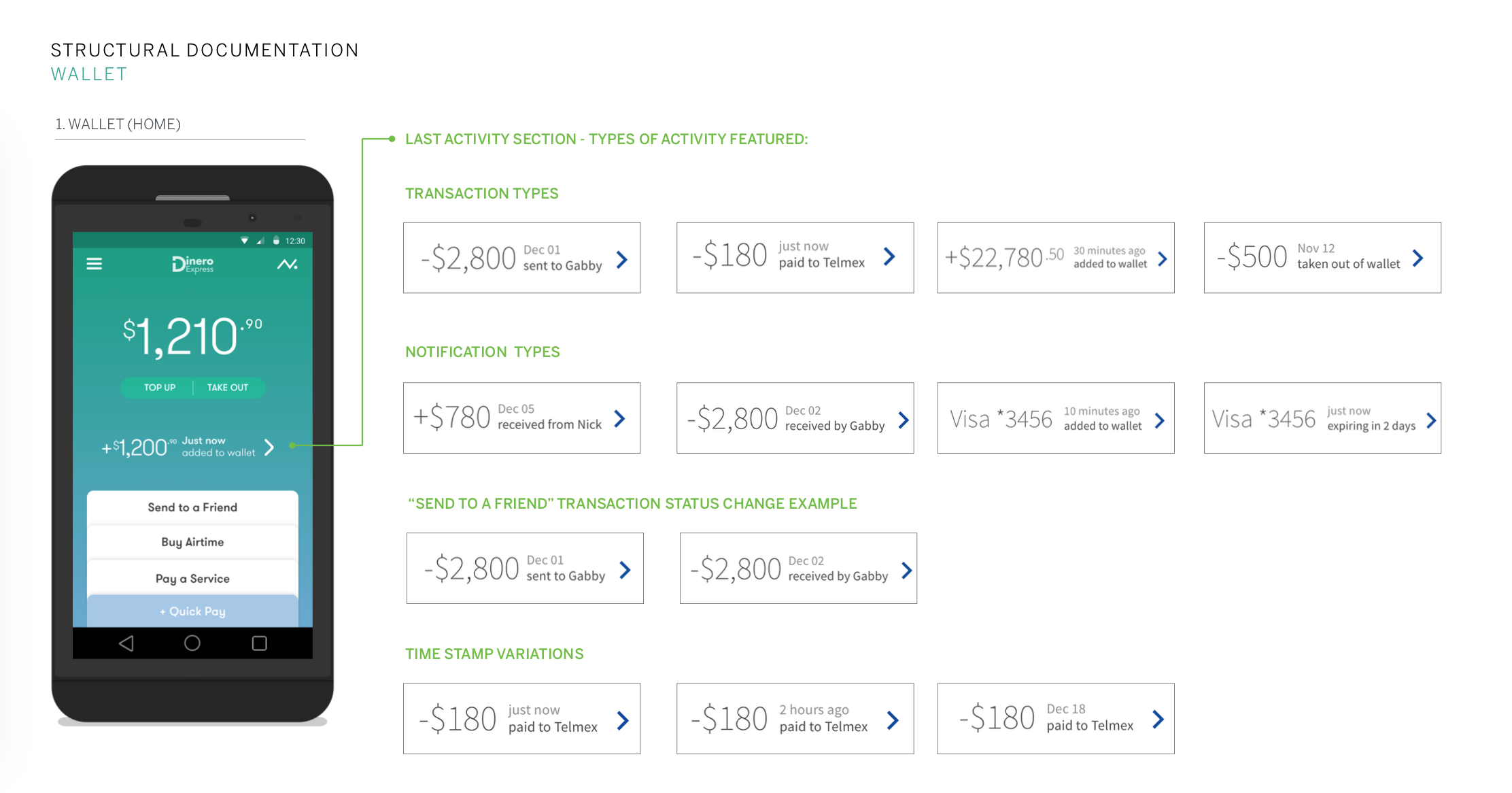

On the 3 layered interaction model, first layer is the base with home and activity feed.

I proposed this structure because we learned how important it is for users to know their money is safe first and foremost. This way when they launch the app, user immediately sees how much money they have, the last transaction that occurred and can immediately start a key transactional flow.

I placed activity feed on the same level, only a tap or swipe away. This feed surfaces users’ money movement (receipts, status of sent and received money with their community). And easy access enables user to know when a loved one picks up money from a retail location.

Hand holding during the unfamiliar first use

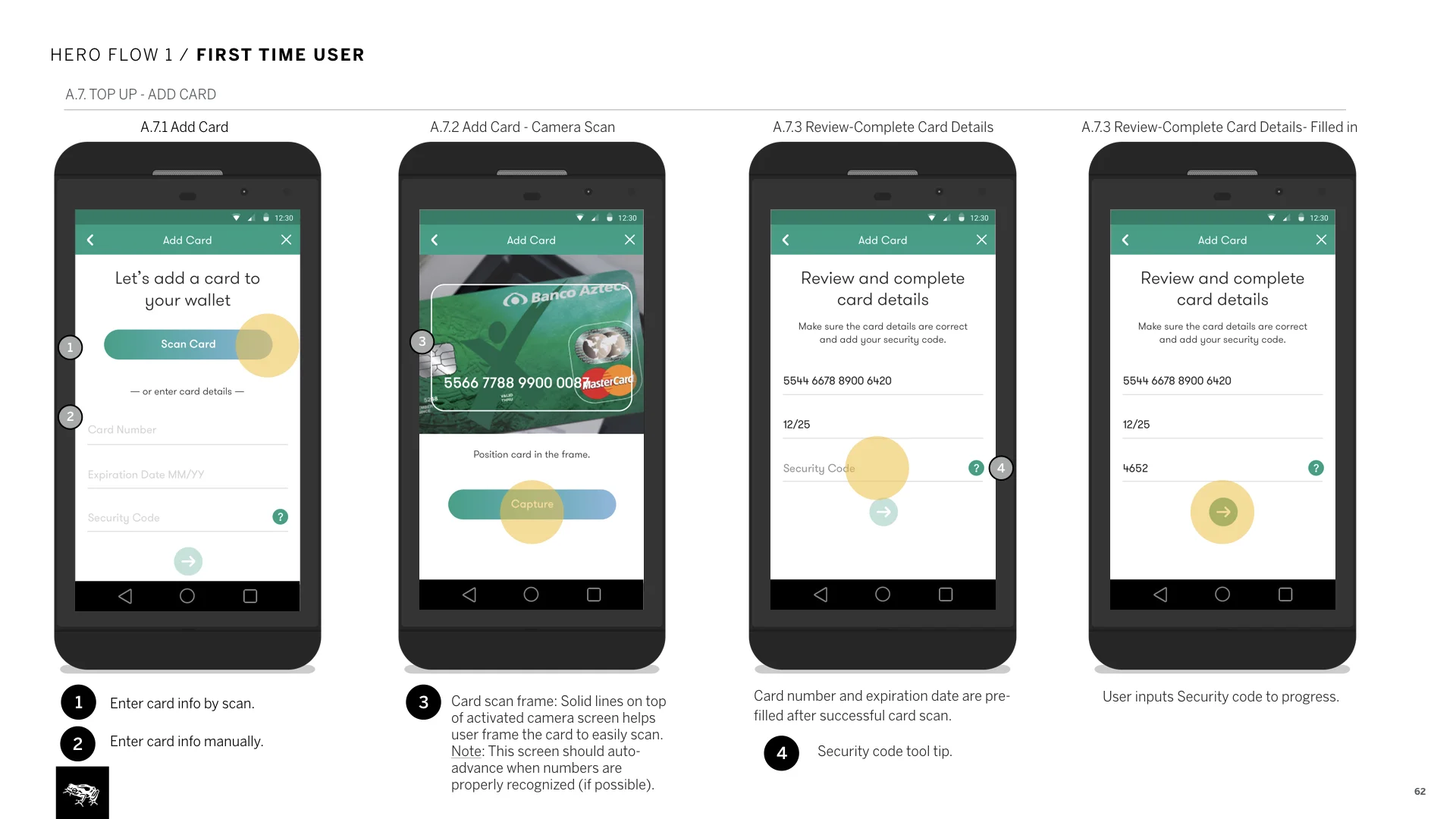

Top layer on the interaction model is transactional flows that occur on modal windows, letting user focus on the complex flows.

All transactional flows feature progressive forms, making sure users see all details in one screen and pursue without errors or confusion.

We also added an informational screen that appear the first time a transactional flow is initiated. Providing clarity to an unfamiliar experience, helping user feel at ease to continue.

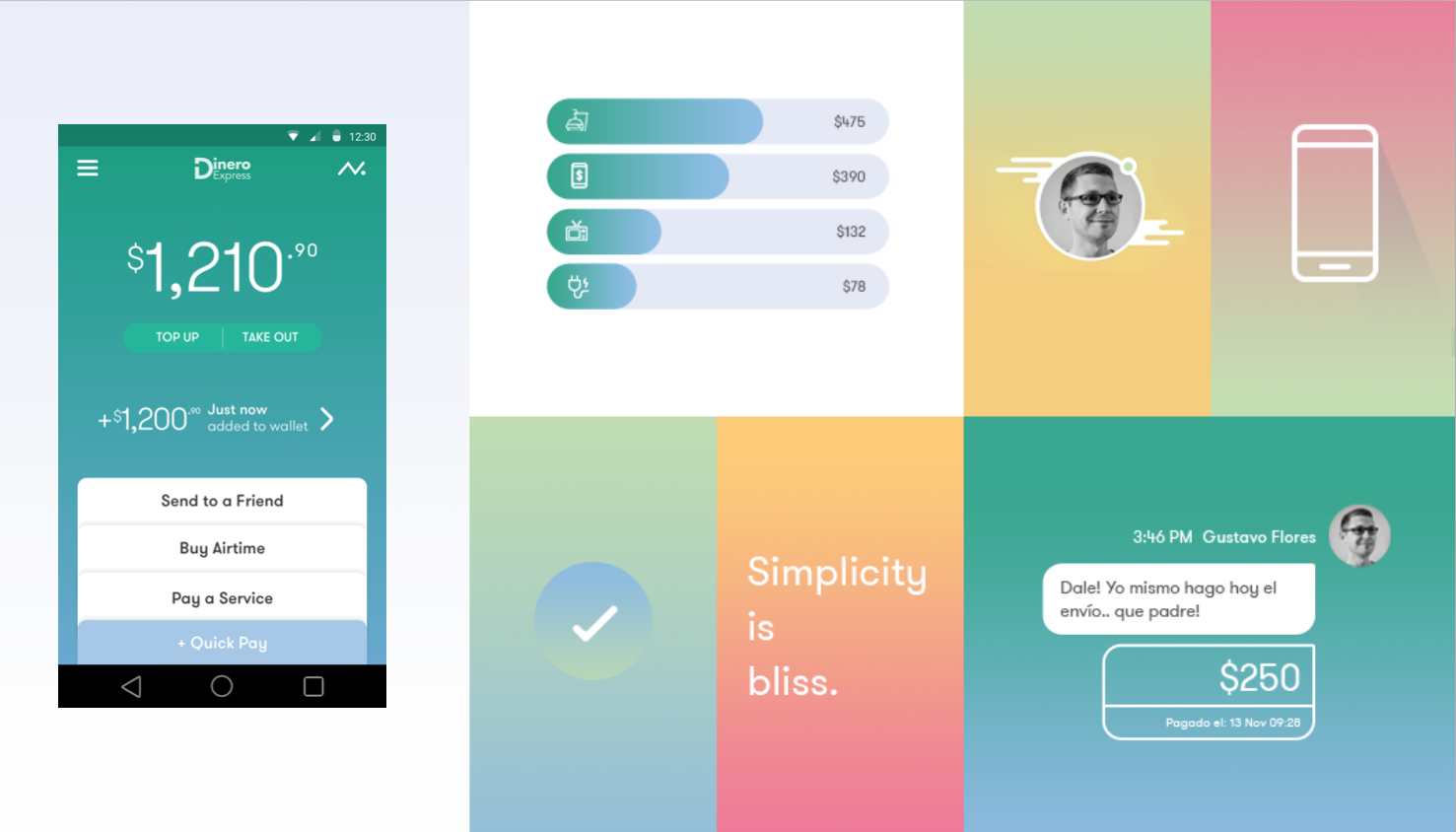

Reassuring the user

Upon submission of a transactional form, animations surface quick details about the action in progress. I realized there was processing and loading times that could be long due to slower connections. Wanting to use the lag in favor of the user, I proposed to reassure them of the progress via informational animations.

Skeuomorphic receipts are also used as proof and record of the money movement.

3. Documentation samples for client

A few sample pages from the documentation I created to help client build the apps. This work was scoped to just a few days, so I chose to provide details on key architecture and UI elements. My efforts helped document design intent clearly, so clients could easily use the agnostic design language to develop the iOS app on their own.

What’s next?

One learning from our market research has been the lower rates of app usage in Mexico, correlated with smartphone ownership. Successful launch of the Android and iOS apps (signaling user acceptance) brought Banco Azteco back to collaborate with us further. We did another round of design for a responsive design system. Banco Azteco is working on developing it, providing even more unbanked users access without the need of a smartphone.